1.0 Introduction

1.1 Corporate governance is the system by which a local authority directs and controls its functions and relates to the community it serves. It is therefore a framework of policies, management systems, procedures and structures that together, determine and control the way in which a local authority manages its business, determines its strategies and objectives, and sets about delivering its services to meet those objectives for the greater good of its community. This naturally extends to how the organisation accounts to, engages with and, where appropriate, leads its community.

1.2 On this basis, the principles of good corporate governance require a local authority to undertake its functions in a way that is completely open and inclusive of all sectors of the community, demonstrates the utmost integrity in all its dealings, and is fully accountable to the public it serves.

1.3 North Yorkshire Council is committed to demonstrating good corporate governance. This code which is based upon the CIPFA/SOLACE document entitled Delivering Good Governance in Local Government: Framework 2016 sets out what the governance arrangements are, and who is responsible for them within the council. It also explains how the arrangements will be kept under review and monitored for compliance.

1.4 The code also expresses how the council will seek to conduct its business in a way that demonstrates –

Openness and inclusivity

Which is necessary to ensure that stakeholders can have confidence in the decision-making and management processes of the council, and the role of the members and officers therein. Being open through genuine consultation with stakeholders and providing access to full, accurate and clear information leads to effective and timely action and lends itself to necessary scrutiny. Openness also requires an inclusive approach, which seeks to ensure that all stakeholders, and potential stakeholders, have the opportunity to engage effectively with the decision-making processes and actions of the council. It requires an outward looking perspective and a commitment to partnership working, that encourages innovative approaches to consultation and to service provision

Integrity

Is necessary for trust in decision making and actions. It is based upon honesty, selflessness and objectivity, and high standards of propriety and probity in the stewardship of public funds and the management of the councils affairs. It is dependent on the effectiveness of the internal control framework and on the personal standards and professionalism of both members and officers. It is reflected in the council's decision-making procedures, in its service delivery and in the quality of its financial and performance reporting

Accountability

Is the process whereby members and officers within the council are responsible for their decisions and actions, including their stewardship of public funds and all aspects of performance, and submit themselves to appropriate external scrutiny. It is achieved by all parties having a clear understanding of those responsibilities, and having clearly defined roles expressed through a robust and resilient structure.

2.0 Policy statement on corporate governance

2.1 The policy of the council is to incorporate the principles of Corporate Governance into all aspects of its business activities to ensure that stakeholders can have confidence in the decision-making and management processes of the authority, and in the conduct and professionalism of its Members, Officers and agents in delivering services. To this end, the council will report annually on its intentions, performance and financial position, as well as on the arrangements in place to ensure good governance is always exercised and maintained.

2.2 The principles set out in this Policy will also apply to the North Yorkshire Pension Fund. Any company in which the council has a substantive equity holding will also be expected to comply with these principles.

3.0 The seven principles of corporate governance

3.1 There are seven core principles that should underpin governance arrangements within a local authority. These are defined as follows –

- Behaving with integrity, demonstrating strong commitment to ethical values, and respecting the rule of law

- Ensuring openness and comprehensive stakeholder engagement

- Defining outcomes in terms of sustainable economic, social, and environmental benefits

- Determining the interventions necessary to optimise the achievement of the intended outcomes

- Developing the entity’s capacity, including the capability of its leadership and the individuals within it

- Managing risks and performance through robust internal control and strong public financial management

- Implementing good practices in transparency, reporting, and audit to deliver effective accountability

3.2 This code addresses these seven core principles and describes the systems and processes that support these in the council. In addition the code reflects how the council addresses the requirements of the CIPFA Statement on the Role of the Chief Financial Officer in Local Government (2015) and the CIPFA Statement on the Role of the Head of Internal Audit (2019).

3.3 The code also explains how the council intends to monitor and review the corporate governance arrangements defined in these codes, including conformance with both CIPFA Statements.

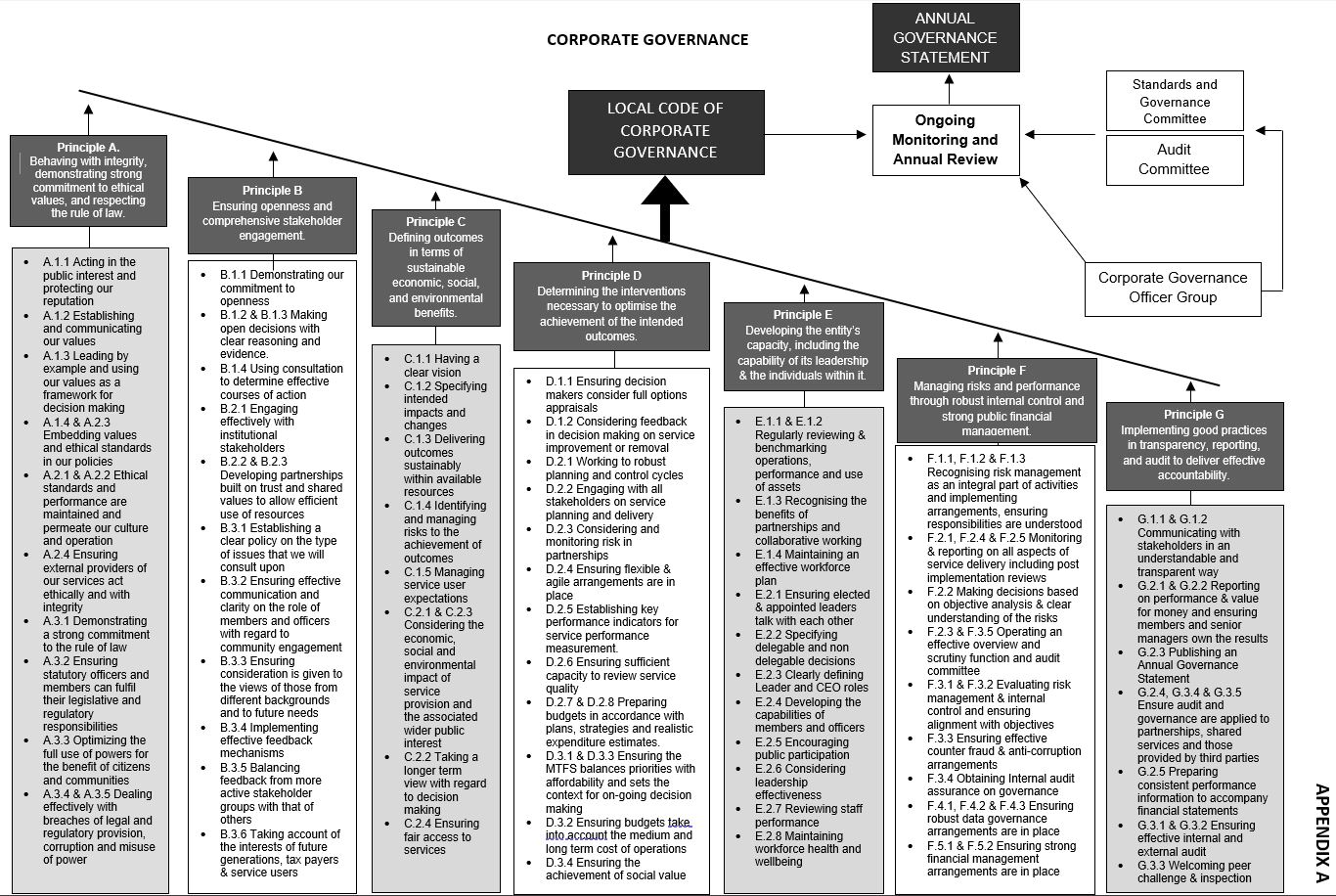

3.4 A diagrammatic representation of how this code fits into the management process of the council is attached as Appendix A.

4.0 corporate governance arrangements

Core principle A: behaving with integrity, demonstrating strong commitment to ethical values, and respecting the rule of law

4.1 The council will conduct its activities in a manner which promotes high ethical standards and good behaviour which will foster openness, support and mutual respect. The following policies and protocols have been established and will be kept under review to assist the council in maintaining this culture:–

- council constitution

- scheme of delegation

- job evaluation scheme

- values and behaviour framework

- councillors’ code of conduct (incorporating the general principles of public life)

- officers’ standards of conduct procedure

- local / national teachers’ code of conduct

- protocol on officer/member relations and communications

- code of conduct for planning

- ethical behaviour statement

- council

- leader

- chief executive

- protocol re the role of the leader and chief executive officer in the ethical framework

- ethical standards and decision making training for officers and members

- twice yearly standards bulletins, circulated to members, officers, certain other authorities and published on the council’s website

- member and officer registers of interests

- member and officer registers of gifts and hospitality

- ICT code of practice and protocols on ICT use for members and officers

- whistleblowing policy

- counter fraud and corruption policy (pdf / 365 KB)

- anti-money laundering and terrorist financing policy (pdf / 400 KB)

- equality, diversity and inclusion policy statement

- communication strategy to support the organisation whilst it is going through transformation

- engagement promise

- partnership governance guidance

- information governance policy and framework

- corporate complaints procedure

- guidance note for councillors and officers on outside bodies

- modern slavery statement

- procurement and contract management strategy

- procurement framework and supply chain resilience board to implement a managed corporate approach with supply chains including financial assistance where appropriate

4.2 In addition, the council will ensure that systems and processes for financial administration, financial control and protection of the authority’s resources and assets are designed in conformity with appropriate ethical standards and monitor their continuing effectiveness in practice. This includes compliance with CIPFA’s Statement on the Role of the Chief Financial Officer in Local Government (2015).

4.3 The aim is to develop a set of shared values which will underpin an ethos of good governance. This will be further supported by compliance with legislation, Procedure Rules and all relevant professional standards.

4.4 The council has established a standards and governance committee to discharge its responsibilities for promoting and maintaining high standards of Member conduct. The Standards and Governance Committee meets twice yearly and as required. It develops initiatives to promote high ethical standards, is involved in ensuring the training of all Members on standards, and determines any complaints that Members may have breached the Members’ Code of Conduct referred to it by the Monitoring Officer. The Committee also has a role in assisting, where requested, in the designation and handling of persistent and/or vexatious complaints/complainants.

4.5 Where the council works in partnership it will continue to uphold its own ethical standards, as well as acting in accordance with the partnership’s shared values and aspirations.

4.6 Where the council has established owned/controlled companies it will put appropriate governance arrangements in place including a governance framework and a register of interests.

Core principle B: ensuring openness and comprehensive stakeholder engagement

4.7 the council will seek the views of its stakeholders and respond appropriately by:–

- clearly identifying its stakeholders, in order to ensure that relationships with these groups continue to be effective

- maintaining effective channels of communication which reach all groups within the community and other stakeholders as well as offering a range of consultation methods; to this end the council has a communications strategy and an engagement promise that are regularly reviewed and updated

- publishing a council plan and an annual statement of final accounts to inform stakeholders and services users of the previous year’s achievements and outcomes

- publishing a medium term financial strategy and consulting each year on the annual revenue budget and its impact on council tax

- providing a variety of opportunities for the public to engage effectively with the council including attending meetings, opportunity to ask questions at meetings, written consultations and surveys

- presenting itself in an open and accessible manner to ensure that council matters are dealt with transparently, in so far as the need for confidentiality allows

- maintaining a freedom of information act publication scheme and arrangements to respond to requests for information from the public

- operating access to information procedure rules to ensure local people and stakeholders can exercise their rights to express an opinion on decisions, and can understand what decisions have been made and why

- ensuring the lawful and correct treatment of personal information through a data protection policy framework that follows the principles set out in the data protection act 2018 and the UK general data protection regulation. how we use data including privacy, freedom of information, data protection, information security, and subject access requests

- maintaining a council website that provides access to information and services and opportunities for public engagement

conformance with the requirements of the local government transparency code - equality, diversity, and inclusion policy statement

Core principle C: defining outcomes in terms of sustainable economic, social, and environmental benefits

4.8 The council will develop a clear vision and purpose, identify intended outcomes and ensure that these are clearly communicated to all stakeholders of the organisation, both internal and external. In doing so, the council will report regularly on its activities and achievements, and its financial position and performance.

4.9 The council will publish:-

- a council plan (looking forward 4 years and updated annually)

- an annual statement of final accounts together with the annual governance statement

4.10 The council will keep its corporate strategies, objectives and priorities under constant review, so as to ensure that they remain relevant to the needs and aspirations of the community.

4.11 In undertaking all its activities, the council will aim to deliver high quality services which meet the needs of service users. Delivery may be made directly, via a subsidiary company, in partnership with other organisations, or by a commissioning arrangement. Measurement of service quality will also be a key feature of service delivery.

4.12 In addition, the council will continue to monitor the cost effectiveness and efficiency of its service delivery, as well as

- ensure that timely, accurate and impartial financial advice and information is provided to assist in decision making and to ensure that the council meets its policy and service objectives and provides effective stewardship of public money in its use

- ensure that the council maintains a prudential financial framework; keeps its commitments in balance with available resources; monitors income and expenditure levels to ensure that this balance is maintained and takes corrective action when necessary

- ensure compliance with CIPFA’s code on prudential framework for Local Authority Capital Finance and CIPFA’s treasury management code

4.13 The council will monitor and regularly report on performance through the Performance Management Framework and system

4.14 The council has a climate change strategy and action plan.

4.15 The council will also seek to address any concerns or failings in service delivery by adhering to and promoting its corporate complaints procedure.

4.16 The council complies with the Public Services (Social Value) Act 2012 ensuring that economic, social, and environmental impact of policies are included in everything it does, and linking economic and social growth with maximising the value obtained from money spent. This is achieved through the procurement and contract management strategy.

Core principle D: Determining the interventions necessary to optimise the achievement of the intended outcome

4.17 The council will observe this Principle through a combination of the following:-

- having a formal constitution which details the decision making processes and the procedures required to support the transparency and accountability of decisions made

- carrying out consultations to ensure a robust decision making process for service improvement or termination or otherwise, in order to prioritise competing demands within limited resources

- publishing a council plan which provides the key ambitions for the council, key strategies, high level outcomes and priorities for the next four years

- publishing an annual statement of final accounts including an annual governance statement to inform stakeholders and services users of the previous year’s achievements and improvements for the following year

- establishing a medium term business and financial planning process to deliver strategic objectives which is reviewed regularly

- maintaining an effective Performance Management Strategy and system

- having a Staff Engagement Strategy

- having a Communications Strategy

- public consultations on key decisions/changes to Policy

Core principle E: Developing the entity’s capacity, including the capability of its leadership and the individuals within it

4.18 The council is continually seeking to develop the capacity and capability of the council itself, and both its members and officers in recognition that the people who direct and control the organisation must have the right skills. This is achieved through a commitment to training and development, as well as recruiting senior officers with the appropriate balance of knowledge and experience. The council aims to achieve this by:-

- maintaining partnership governance procedures and guidance, and carrying out regular reviews of partnerships and their outcomes

- organising member and employee induction programmes

- scheme of delegation for members and officers

- continuing with further organisational development

- maintaining an effective performance management strategy and system

- continuing to develop a workforce plan that addresses issues such as recruitment, succession planning, flexible working and other people management issues including an online recruitment and induction process, and online learning on leading and managing remote teams

- carrying out regular appraisals which incorporate service improvement and personal development plans

- providing career structures to encourage staff development

- regularly reviewing job descriptions and person specifications and using these as the basis for recruitment

- encouraging a wide variety of individuals and organisations to participate in the work of the council, including through a volunteer strategy

- ensuring regular review and improvement of “health assured” for employees which includes health assessments, counselling, emotional

support and fitness advice - providing apprenticeship schemes

4.19 To ensure compliance with the CIPFA Statement on the role of the Chief Financial Officer the council will:-

- ensure the CFO has the skills, knowledge, experience and resources to perform effectively in both the financial and non-financial areas of his role

- review the scope of the CFO’s other management responsibilities to ensure financial matters are not compromised

- provide the finance function with the resources, expertise and systems necessary to perform its role effectively

- embed financial competencies in person specifications and appraisals

- ensure that Members’ roles and responsibilities for monitoring financial performance / budget management are clear, that they have adequate

- access to financial skills and are provided with appropriate financial training on an ongoing basis to help them discharge their responsibilities

4.20 To ensure conformance with the CIPFA Statement on the Role of the Head of Internal Audit the council will ensure the HoIA:-

- objectively assesses the adequacy and effectiveness of governance and management of risks, giving an evidence based opinion on all aspects of governance, risk management and internal control

- champions best practice in governance and commenting on responses to emerging risks and proposed developments

- is a senior manager or equivalent with regular and open engagement across the organisation, particularly with management board and with the audit committee

- leads and directs an internal audit service that is resourced appropriately, sufficiently and effectively

- is professionally qualified and suitably experienced

Core principle F: Managing risks and performance through robust internal control and strong public financial management

4.21 The council observes this Principle through a combination of the following:-

- a risk management policy (pdf / 280 KB) and procedures have been in place for many years and are reviewed and updated in line with current guidance and best practice on a regular basis

- there is a reporting and monitoring framework for communicating risks (for example, corporate risk management and resilience group/directorate risk management and resilience group/service management teams)

- decision making is supported through risk registers at corporate, directorate and service levels as well as one-off major projects

- risk registers with clear risk owners include consideration of objectives and contribute to service plans and performance

- there is a corporate performance management strategy and system including greater use of performance dashboards

- the executive is supported at all times by professional advice that addresses all relevant legal, financial, risk and resourcing issues

- risk management processes operate so as to ensure that the risk and impact of decisions are fully assessed

- there are regular quarterly performance / financial reports to executive and scrutiny board

- there is a year-end report on performance / financial out-turn to executive and scrutiny board

- there is comprehensive recording of all decisions taken and the reasons for those decisions

- there is an effective scrutiny function and framework, supported by named officers, that enables decisions by the executive to be challenged or influenced by the rest of the council’s members

- there is compliance with the code of practice on managing the risk of fraud and corruption (CIPFA 2014) through a counter fraud policy and strategy including a fraud prosecution policy, and an anti-money laundering policy and procedures. the counter fraud strategy is aligned with the national fighting fraud and corruption strategy

- there is a local code of corporate governance (this document) as well as an annual governance statement which is updated and forms part of the annual statement of final accounts

- the audit committee includes independent co-opted members

- there is an information governance policy framework which ensures compliance with data protection and access to information legislation and best practice

- an information sharing protocol has been agreed with all key partners and individual agreements are in place where personal data is shared there is an audit charter with an adequately resourced internal audit and counter fraud function

- governance arrangements allow the cfo direct access to the audit committee and external auditor

- by ensuring the provision of clear, well presented, timely, complete and accurate information and reports to budget managers and senior officers on the budgetary and financial performance of the council

- by ensuring the council’s governance arrangements allow the cfo to bring influence to bear on all material decisions

- by ensuring that advice is provided on the levels of reserves and balances in line with good practice guidance

- the council's arrangements for financial and internal control and for managing risk are addressed in annual governance reports by corporate directors to the audit committee

- the council puts in place effective internal financial controls covering codified guidance, budgetary systems, supervision, management review and monitoring, physical safeguards, segregation of duties, accounting procedures, information systems and authorisation and approval processes

- business continuity framework

- emergency response plan/ command and control structure

Core principle G: Implementing good practices in transparency, reporting, and audit to deliver effective accountability

4.22 The council observes this Principle through a combination of the following:-

- conformance with the requirements of the Local Government Transparency Code

- maintaining a council website that provides access to information and services and opportunities for public engagement

- all meetings of the council and its committees are open to the public, broadcasted live and recordings published on the internet (except where, for example, personal or confidential matters are being discussed)

- having a formal constitution which details the decision making processes and the procedures required to support the transparency and accountability of decisions made

- an engagement promise setting out in simple terms how everyone who lives or works in the county, or uses the council’s services can influence decisions

- a properly constituted standards and governance committee, an Audit Committee with a number of independent co-opted members and an effective scrutiny function

- there is an Audit Charter with an adequately resourced internal audit function which conforms to the Public Sector Internal Audit Standards and professional best practice (including the CIPFA Statement on the Role of the Head of Internal Audit 2019)

- by maintaining an effective counter fraud and corruption policy (pdf / 365 KB) framework and an adequately resourced counter fraud function

- by ensuring that its governance arrangements allow the CFO direct access to the Audit Committee and External Auditor

- by ensuring the provision of clear, well presented, timely, complete and accurate information and reports to budget managers and senior officers on the budgetary and financial performance of the authority

- by ensuring the council’s governance arrangements allow the CFO to bring influence to bear on all material decisions

- ensure that advice is provided on the levels of reserves and balances in line with good practice guidance

- by ensuring the council puts in place effective internal financial controls covering codified guidance, budgetary systems, supervision, management review and monitoring, physical safeguards, segregation of duties, accounting procedures, information systems and authorisation and approval processes

- ensuring the council’s arrangements for financial and internal control and for managing risk are addressed in annual governance reports by Corporate Directors to the Audit Committee

- publishing an annual Statement of Final Accounts together with the Annual Governance Statement which will show any significant improvements required.

- completion of equality impact assessments / Data Protection Impact Assessments and Climate Impact Assessments for any proposed changes in policy or service delivery

5.0 monitoring, reporting and review

5.1 Ensuring good corporate governance is the responsibility of the whole council. However to formalise the process, the council has two committees that are primarily responsible for monitoring and reviewing the adequacy of the corporate governance arrangements referred to in this local code+ –

The two committees liaise on any issue of Corporate Governance that may be of legitimate common concern to both.

5.2 The audit committee is independent of both the Executive and Scrutiny, and has wide ranging responsibilities in relation to audit, information governance, counter fraud, risk management, treasury management, financial and performance reporting, as well as overall corporate governance and ethics. The Committee’s terms of reference are set out in the Constitution and its principal objectives are to ensure that the council manages its risks appropriately and maintains an adequate and effective system of internal control. The committee meets up to five times a year and includes up to three co-opted external Members.

5.3 The standards and governance committee currently meets twice yearly and as required to promote and maintain high standards of conduct by councillors and co-opted Members of the council. The Committee provides advice and support to the council and its members on the council’s Members’ Code of Conduct and related ethical issues such as membership of outside bodies and Member/officer relations. Additionally, Standards and Governance Committee Members participate in training sessions and the Committee determines any complaints that Members may have breached the Members’ Code of Conduct referred to it by the Monitoring Officer. The Committee also has a role in assisting, where requested, in the designation and handling of persistent and/or vexatious complaints/complainants. The Committee is attended by independent persons, as well as council members.

5.4 Further to the two committees referred to above, the council has also established:

- a corporate governance officer group of senior officers, chaired by the corporate director of resources, which is responsible for overseeing the delivery of an integrated programme of work to support the development of robust corporate governance arrangements, and to keep implementation of such arrangements under on-going review - in particular, this group monitors the self-assessment checklist that maps, and monitors, all governance activity within the council against all published best practice guidelines

- a corporate information governance group, also chaired by the corporate director of resources - this group addresses the various challenges of information governance including the development and maintenance of a framework for information governance which comprises a suite of relevant policies, protocols and guidance notes

5.5 The council is required to undertake an annual review of the effectiveness of its system of internal control (as required by Regulation 6 of the Accounts and Audit Regulations (2015). This review seeks to –

- identify principal risks to the achievement of council objectives

- identify and evaluate key controls to manage principal risks

- obtain assurances of the effectiveness of key controls

- evaluate assurances and identify gaps in control/assurances

This review is overseen by the audit committee and is part of the preparatory process for the annual governance statement (see paragraph 5.8 below). The Audit Committee receives assurance from various sources regarding the adequacy of the internal control environment and overall corporate governance arrangements, including from the Head of Internal Audit.

5.6 Additionally, compliance with the CIPFA Statement on the Role of the Chief Financial Officer in Local Government is reviewed annually by the Audit Committee.

5.7 Finally, annual reports are produced and published by:

The annual governance statement

5.8 Following the annual review of effectiveness of the system of internal control an Annual Governance Statement (AGS) will be published to accompany the Statement of Final Accounts for the council. The AGS will provide an overall assessment of the corporate governance arrangements in the council.

5.9 To reflect the council’s commitment to the continuous improvement of its system of internal control, progress to address weaknesses is drawn up in response to any significant control weaknesses identified in the AGS. A follow up process is then overseen by the Corporate Governance Officer Group to ensure continuous improvement of the system of corporate governance. The Audit Committee monitors progress to address weaknesses.

Review of this code

5.10 A review of this code will be undertaken annually alongside the preparation of the AGS.

6.0 Contact details and further information

6.1 Further details of the council’s corporate governance arrangements can be obtained on our website or by contacting the corporate director of resources.

6.2 Finally, if you have any concerns about the way in which the council, its Members, Officers or agents conduct its business, or believe that elements of this code are not being complied with, please contact one of the following Officers as appropriate. Your enquiry will be treated confidentially, and a response made following investigation of the facts in each case.

(i) Chief Executive (Head of Paid Service)

Richard Flinton

North Yorkshire Council

County Hall

Northallerton

North Yorkshire DL7 8AL

Tel: 01609 532444

E-mail: richard.flinton@northyorks.gov.uk

(ii) Corporate Director of Resources (Section 151 Officer)

Gary Fielding

Corporate Director of Resources

North Yorkshire Council

County Hall

Northallerton

North Yorkshire DL7 8AL

Tel: 01609 533304

E-mail: gary.fielding@northyorks.gov.uk

(iii) Assistant Chief Executive Legal and Democratic Services

(Monitoring Officer)

Barry Khan

Legal and Democratic Services

North Yorkshire Council

County Hall

Northallerton DL7 8AL

Tel: 01609 532173

E-mail: barry.khan@northyorks.gov.uk

Appendix A